A Balanced Approach

May 2022

In the last quarter-century, we have directly experienced two brief periods when balanced funds were labeled obsolete. Both times occurred after a long bull market in stocks.

The most memorable time was in late 1999. We had put together balanced accounts for institutional investors averaging about 65% in stocks, with the remainder in bonds and cash. They were appreciating nicely, but not as fast as tech stocks in the momentum-driven market at the time.

I vividly recall two searing experiences with clients.

In the first instance, I conducted a review with a group of physicians in Ohio. I had managed their money for several years and came to the meeting very pleased to have invested them in a really fine balanced portfolio. The lead doctor looked at me as though I did not exist, that I was not a serious investment manager. I was humiliated. They fired us the next day and split the portfolio between two investment managers. Both managers invested all of the money in the red-hot telecom sector; both managers experienced portfolio declines of about 90% over the next two years. I do not believe the doctors ever recovered from those catastrophic losses.

The second instance eventually turned out positively. I conducted a review with another set of doctors from Iowa. They told me that I did not know how to invest in growth stocks. I was incensed. I am embarrassed to admit that I lost my temper. I believed their criticism was unfair. Ultimately, cooler heads prevailed, and they did not terminate us. Four years later after a portfolio review, the senior physician followed me out to my car. He thanked me. He said our adherence to our process both on stocks and bonds had protected the long-term viability of their investment assets.

Both incidents reinforce the wisdom and value of a balanced portfolio. They also beg the question: If long-running bull markets end to make balanced portfolios seem obsolete, why haven’t they become a relic? In this age of heavily promoted, “sophisticated volatility management solutions,” Wall Street has relentlessly promoted tactics that diversify investments into thousands of global stocks and bonds across a dozen or more mutual funds. The obvious answer is that balanced portfolios endure because they are a far better solution for most investors.

In our view, balanced portfolios offer six key benefits to investors:

1 A BALANCED PORTFOLIO IS AN ALL-WEATHER PORTFOLIO

It offers a solid potential for reasonable long-term returns with less volatility than an all-stock portfolio. When we set up the DGI Fund, we had a long-term return target of 10% per year. We believed we could earn 12%-plus on the stocks and 3%-4% on fixed income securities. Since the Fund’s inception (August 12, 2011 ), we have overachieved, earning a return of 12.90% per year through December 31, 2021, after fees. The primary basis for the excess return over our target was the performance of the stock portfolio. Our investment management was highly effective, both absolutely and relative to the S&P 500. The stocks increased at 17.7% per year, exceeding the return from the S&P 500, which increased at 16.7% per year. The bond portion of the mutual fund increased at 3.8% per year, in line with our target.

What about annual volatility? As of December 31, 2021, the DGI Fund was slightly more than 10 years old. During eight of those 10 calendar years, the Fund earned a positive return. The other two years, 2015 and 2018, the Fund suffered losses of 4.6% in 2015 and 2.4% in 2018. This is a normal ratio of winning/losing years for a balanced account. The severity of down markets can be greatly reduced in a balanced portfolio as well. In the last 93 calendar years, The S&P 500 has declined in 25 of those years. During these down years, a hypothetical balanced portfolio of 65% S&P 500 stocks and 35% US Treasury Bonds would have declined just 40% of the amount of the all-stock portfolio, on average.1 Declines are inevitable. An investor holding a balanced portfolio can reasonably expect materially less severe declines than an investor holding an all-stock portfolio. Occasionally, holding a balanced portfolio will even produce positive results in a year where the allstock portfolio declines.

2 A BALANCED PORTFOLIO GUIDES THE INVESTOR TO THE PROPER LONG-TERM MIX DF ASSETS

We believe it’s smart investing to establish a long-term target mix of assets. The objective in establishing this target mix is to determine the mix of assets that offers reasonable odds of achieving a satisfactory long-term return with tolerable annual volatility. For most investor, we think a mix of 65% stocks and 35% bonds is a good fit to achieve reasonable long-term results with bearable peaks and valleys2.

Balanced portfolios have four essential and sustainable advantages for most investors when compared against the common industry approach3:

-

1) Simplicity: For both the investment manager and the client, a straightforward, single portfolio of stocks and bonds leads to simplicity of investment goals, simplicity of process, and simplicity of products instead of esoteric, overly complex offerings manufactured by Wall Street4.

-

2) Transparency: In a single portfolio, clients can be fully informed of their investments. This leads to more productive conversations between manager and client. Similarly, performance on the single portfolio is easier to measure and understand, and fees are calculated on one portfolio instead of multiple products with varying fee structures5.

-

3) Cost Effectiveness: Balanced funds should be easily managed at a lower cost than all-stock portfolios or a mix of varying products. We believe that the fees to manage bonds should be lower than that for managing stocks, so investors in a balanced portfolio may benefit in this way.

-

4) True Diversification: As detailed in this article, stocks and bonds exhibit materially different returns behavior. Owning different baskets of stocks based on geographic location, industry, etc. does not produce the same effect, despite the investment industry’s claims. As an example, the MSCI ex-USA index represents 85% of the market value of 22 out of 23 developed countries, excluding the USA. During the bear market of 2008, this index suffered a loss of 39.3%. The S&P 500 suffered a loss of 38.5%. During the first quarter of 2020, the MSCI ex-USA index declined by 20.4%. The S&P 500 declined by 19.6%. The point is: all these markets declined to a nearly identical degree, exposing the myth of some material benefit for investors through global diversification of stocks. By contrast, the Barclay’s Gov/Cred Bond Index returned 5.2% during the 2008 bear market and 3.2% during the first quarter of 2020. Similarly, in 35 of the last 94 calendar years, stocks and bonds have performed so differently from each other that one group had an up year while the other had a down year6. More frequently than once every three years either stocks go up and bonds go down, or stocks go down and bonds go up. That degree of diversification in results is not evident between various baskets of stocks.

A target mix of assets can play an important role in long-term investment success. The investor should generally maintain the target mix unless unusual personal circumstances intercede, such as a major health issue requiring high spending. Because the target asset mix is a suitable reference point, investors can measure their current asset mix versus the target. For example, if an investor is invested 40% in stocks and 60% in bonds, this person is in danger of not achieving good long-term results because bonds typically have lower returns. Or if the investor owns 90% stocks and 10% bonds, the investor may be vulnerable to excessive peaks and valleys.

3 A BALANCED PORTFOLIO ALLOWS STOCKS AND BONDS TO BE USED AS INTENDED

Many years ago a brilliant and wise client shared a priceless fundamental truth with me: stocks are for growth and bonds are for income. A balanced portfolio allows the portfolio manager to invest in growth company stocks while still providing reasonable current income from the bonds. By prudently investing in growth companies the investment manager improves the long-term return from the portfolio. By investing a portion of the portfolio in bonds, the manager can achieve current income plus dampen the annual volatility of the portfolio to a level tolerable to most investors. In this way, a balanced portfolio can be geared primarily for growth with bonds providing income and dampening volatility.

Often in our industry, investment managers use complex “volatility management” strategies. These strategies attempt to use stocks for reasons other than growth and bonds for reasons other than income and stability. In our opinion, these approaches do not work. Stocks will behave like stocks and bonds like bonds, and they should be used accordingly.

4 A BALANCED PORTFOLIO ALLOWS THE INVESTOR TO TILT INSTEAD OF PLUNGE

In a serious bear market for stocks, bonds increase in price or decline more modestly than stock prices. This is especially true of investment-grade bonds. It is not uncommon during these markets that the allocation of stocks relative to bonds can drop 5-10 percentage points, say from 65% in stocks to 55%-60%. An investor can tilt the portfolio by rebalancing back to 65% stocks. That is accomplished by selling some bonds and using the proceeds to buy stocks. Conversely, in a bull market for stocks, the exposure to stocks can increase to 70% or 75%. An investor can tilt the portfolio by rebalancing the stocks down to 65%. This has the potential to add materially to the returns on the portfolio and reduce downside volatility.

In 2020, during the Covid-19 bear market, we rebalanced the mutual fund when stocks were down. The low point for equity exposure was 61.1 % on March 16, 2020, a decline from the 70% target we had at the time. On March 17, we started rotating from bonds to stocks. By March 31, we reached 67.4% equities (a 6.3% increase). From March 31 to December 31, 2020, stocks in the Fund returned 74.3% while bonds returned 13.2%. The difference in stock versus bond performance after March 31, 2020 means we added nearly 4% to the Fund’s 2020 total performance with the shift from bonds to stocks.

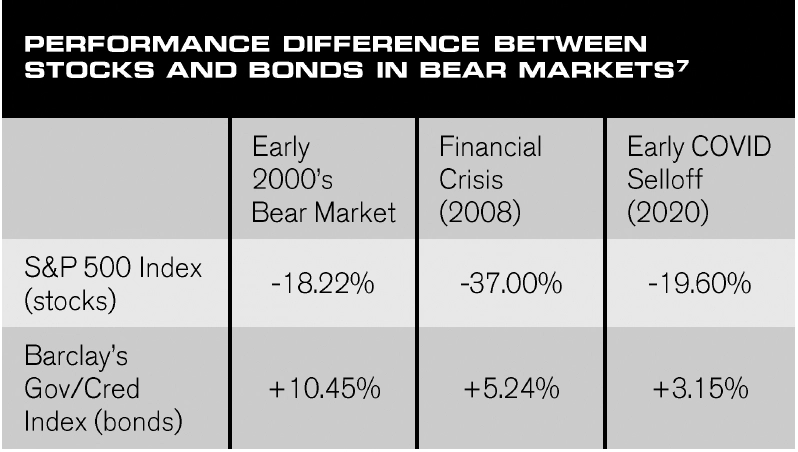

5 A BALANCED PORTFOLIO OFFERS REAL, TIME-TESTED DIVERSIFICATION

Fixed income securities like bonds have always behaved differently from stocks. During bear market activity, stocks decline and bonds generally increase or decline modestly. Bonds and stocks performed as expected during the last three bear markets in 1999-2002 (early 2000’s bear market), 2008 (financial crisis), and 2020 (early COVID selloff). Below you can see the difference in performance between stocks and bonds broadly during these bear markets:

6 AN INVESTOR SHOULD PAY LOWER FEES WITH A BALANCED PORTFOLIO

We priced the fees on the DGI Fund based on its role as a balanced fund. We believe investment portfolio fees should be based on the likely future return from the portfolio. More directly, the higher the expected return, the higher the fee a portfolio can sustain. Since stocks tend to achieve higher long-term return than bonds, it makes sense that investment fees for an all-stock portfolio would be higher than an all-bond portfolio. We think a balanced fund’s fees should be somewhere between an all-stock portfolio or all bonds.

Information Sources & Disclosures

1 The 93-year time frame is presented for historical context and illustrative purposes only. For fixed income securities, The DGI Fund typically invests in both corporate bonds and US Government-issued bonds. Data source: https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

2 Each investor may have a different volatility threshold above which volatility is not “tolerable”. In our experience, most investors can tolerate the volatility of a 65% stock/ 35% bond mix in exchange for the growth it may provide.

3 According to the 2021 Investment Company Institute Fact Book, the median number of funds owned by investors is four. According to Statista, 40% of mutual fund assets were passive/ index funds as of 2020. The average number of stocks held by a mutual fund was 125. With four funds averaging 125 holdings, the median investor owns around 500 stocks, likely more given that index funds have more stocks than active funds, and index funds account for 40% of all fund assets (Statista, 2020).

4 Wall Street’s approaches result in complexity as the number of products used increases and lack of transparency increases. Source/example: https://www.cnbc.com/2022/04/01/investing-may-be-too-complex-for-retail-investors-and-brokers.html

5 As referenced, the median household has 4 mutual funds (2021 ICI Factbook). The median mutual fund has 3 share classes. All US mutual funds aside from three (using Morningstar data) are sold through brokerage platforms which charge fees to both the investment manager and client to access their brokerage services. The fewer things you have to compare and calculate, the easier it is to understand what you pay.

6 Sources: MSCI index data from Morgan Stanley Capital International (MSCI) data sets. Barclay’s Gov/Cred bond index data from Barclay’s. Stock/bond returns data from last 94 years from NYU Stern School of Business: https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

7Source: DGI’s portfolio accounting system using data from Standard & Poor’s and Barclay’s

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please visit www.dgifund.com.

While the goal of diversification is to reduce investment-specific risks, diversification does not guarantee investors will not lose value, including potential loss of value in stocks and bonds in the same period of time such as a calendar year (or, potentially, longer). Similarly, losses in one asset class may offset gains in another and no profit is guaranteed as a result of any degree of diversification.

ALPS Distributors, Inc. is the distributor of The Disciplined Growth Investors Fund.